Genesis Energy Limited's (NZSE:GNE) Stock's Been Going Strong: Could Weak Financials Mean The Market Will Coorect Its Share Price?

Genesis Energy (NZSE:GNE) has had a great run on the share market with its stock up by a significant 12% over the last month. However, we decided to pay close attention to its weak financials as we are doubtful that the current momentum will keep up, given the scenario. In this article, we decided to focus on Genesis Energy's ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for Genesis Energy

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Genesis Energy is:

2.2% = NZ$46m ÷ NZ$2.1b (Based on the trailing twelve months to June 2020).

The 'return' is the amount earned after tax over the last twelve months. So, this means that for every NZ$1 of its shareholder's investments, the company generates a profit of NZ$0.02.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Genesis Energy's Earnings Growth And 2.2% ROE

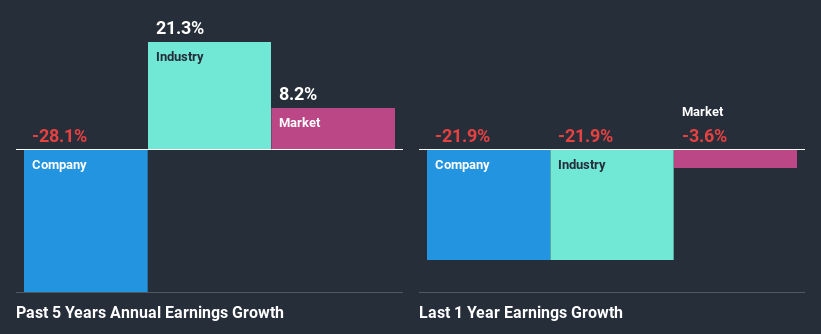

It is quite clear that Genesis Energy's ROE is rather low. Even compared to the average industry ROE of 5.5%, the company's ROE is quite dismal. Therefore, it might not be wrong to say that the five year net income decline of 28% seen by Genesis Energy was possibly a result of it having a lower ROE. We reckon that there could also be other factors at play here. For instance, the company has a very high payout ratio, or is faced with competitive pressures.

However, when we compared Genesis Energy's growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 21% in the same period. This is quite worrisome.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. What is GNE worth today? The intrinsic value infographic in our free research report helps visualize whether GNE is currently mispriced by the market.

Is Genesis Energy Making Efficient Use Of Its Profits?

Genesis Energy's very high three-year median payout ratio of 385% over the last three years suggests that the company is paying its shareholders more than what it is earning and this explains the company's shrinking earnings. Its usually very hard to sustain dividend payments that are higher than reported profits. You can see the 2 risks we have identified for Genesis Energy by visiting our risks dashboard for free on our platform here.

In addition, Genesis Energy has been paying dividends over a period of six years suggesting that keeping up dividend payments is preferred by the management even though earnings have been in decline. Our latest analyst data shows that the future payout ratio of the company is expected to drop to 191% over the next three years. Accordingly, the expected drop in the payout ratio explains the expected increase in the company's ROE to 4.4%, over the same period.

Conclusion

Overall, we would be extremely cautious before making any decision on Genesis Energy. The low ROE, combined with the fact that the company is paying out almost if not all, of its profits as dividends, has resulted in the lack or absence of growth in its earnings. Having said that, looking at current analyst estimates, we found that the company's earnings growth rate is expected to see a huge improvement. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.