Is Tennant Company's (NYSE:TNC) CEO Being Overpaid?

In 2005 H. Killingstad was appointed CEO of Tennant Company (NYSE:TNC). This report will, first, examine the CEO compensation levels in comparison to CEO compensation at companies of similar size. After that, we will consider the growth in the business. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. The aim of all this is to consider the appropriateness of CEO pay levels.

Check out our latest analysis for Tennant

How Does H. Killingstad's Compensation Compare With Similar Sized Companies?

Our data indicates that Tennant Company is worth US$1.1b, and total annual CEO compensation was reported as US$4.9m for the year to December 2019. Notably, that's an increase of 16% over the year before. We think total compensation is more important but we note that the CEO salary is lower, at US$796k. We further remind readers that the CEO may face performance requirements to receive the non-salary part of the total compensation. When we examined a selection of companies with market caps ranging from US$400m to US$1.6b, we found the median CEO total compensation was US$3.2m.

Now let's take a look at the pay mix on an industry and company level to gain a better understanding of where Tennant stands. On an industry level, roughly 17% of total compensation represents salary and 83% is other remuneration. Tennant is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation

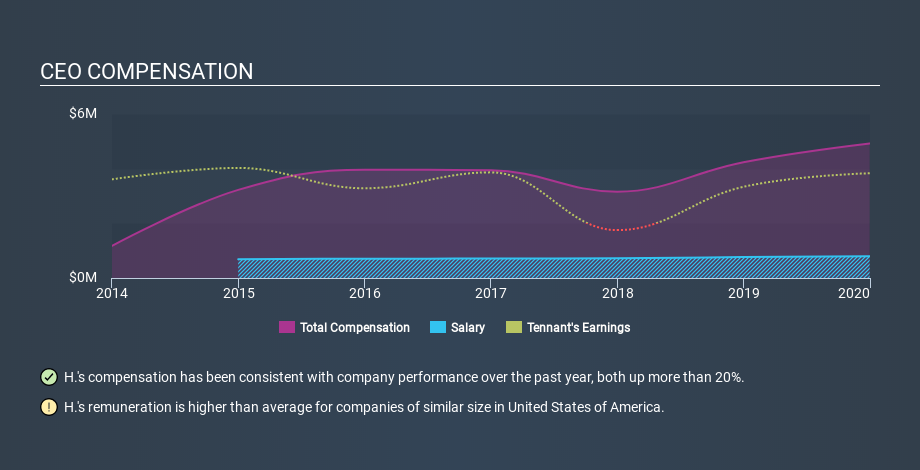

As you can see, H. Killingstad is paid more than the median CEO pay at companies of a similar size, in the same market. However, this does not necessarily mean Tennant Company is paying too much. We can get a better idea of how generous the pay is by looking at the performance of the underlying business. The graphic below shows how CEO compensation at Tennant has changed from year to year.

Is Tennant Company Growing?

Tennant Company has seen earnings per share (EPS) move positively by an average of 19% a year, over the last three years (using a line of best fit). In the last year, its revenue is up 1.3%.

This demonstrates that the company has been improving recently. A good result. It's also good to see modest revenue growth, suggesting the underlying business is healthy. You might want to check this free visual report on analyst forecasts for future earnings.

Has Tennant Company Been A Good Investment?

Given the total loss of 15% over three years, many shareholders in Tennant Company are probably rather dissatisfied, to say the least. So shareholders would probably think the company shouldn't be too generous with CEO compensation.

In Summary...

We compared total CEO remuneration at Tennant Company with the amount paid at companies with a similar market capitalization. As discussed above, we discovered that the company pays more than the median of that group.

However, the earnings per share growth over three years is certainly impressive. However, the returns to investors are far less impressive, over the same period. This doesn't look great when you consider CEO remuneration is up on last year. While EPS is moving in the right direction, we'd say shareholders would want better returns before the CEO is paid much more. Moving away from CEO compensation for the moment, we've identified 2 warning signs for Tennant that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.