Meloni Gets Warning Light as Italian Retail-Bond Demand Wanes

(Bloomberg) -- A warning light for Italy’s finances just flashed for Premier Giorgia Meloni after her government pressed ahead with a debt sale to consumers even though it knew demand would weaken.

Most Read from Bloomberg

Trump Vows ‘Day One’ Executive Order Targeting Offshore Wind

China to Start $138 Billion Bond Sale on Friday to Boost Economy

Putin Names Economist as Defense Minister in Surprise Reshuffle

Global Chips Battle Intensifies With $81 Billion Subsidy Surge

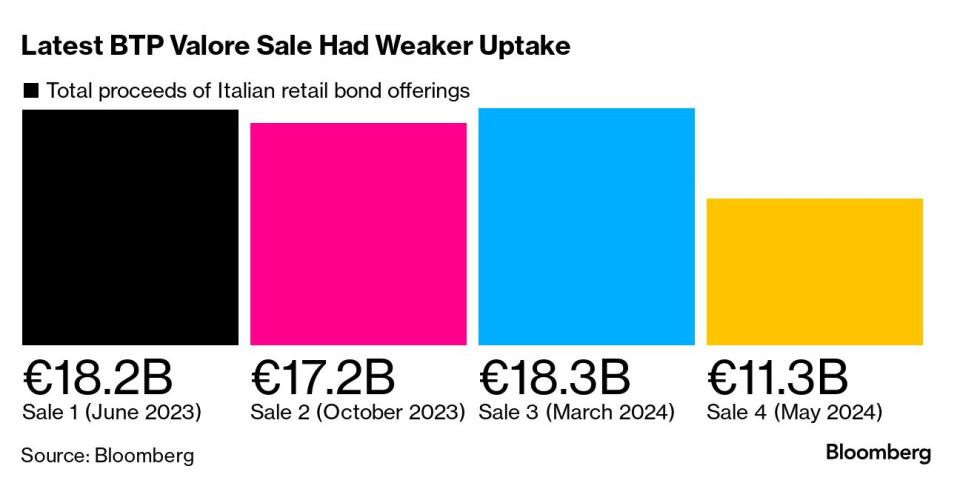

The Treasury held the BTP Valore offering this week despite anticipating less uptake than before because it faced immediate cash needs and didn’t want to tap institutional investors instead, according to people familiar with the matter. They declined to be identified because discussions are confidential.

The sale, which ended on Friday, brought in around €11.3 billion ($12.2 billion), compared with three previous offerings which raised an average just shy of €18 billion each.

Waning enthusiasm from consumers — an increasingly important pillar of Italy’s funding — adds to mounting evidence that the public-finance backdrop of Europe’s second-most indebted country is darkening.

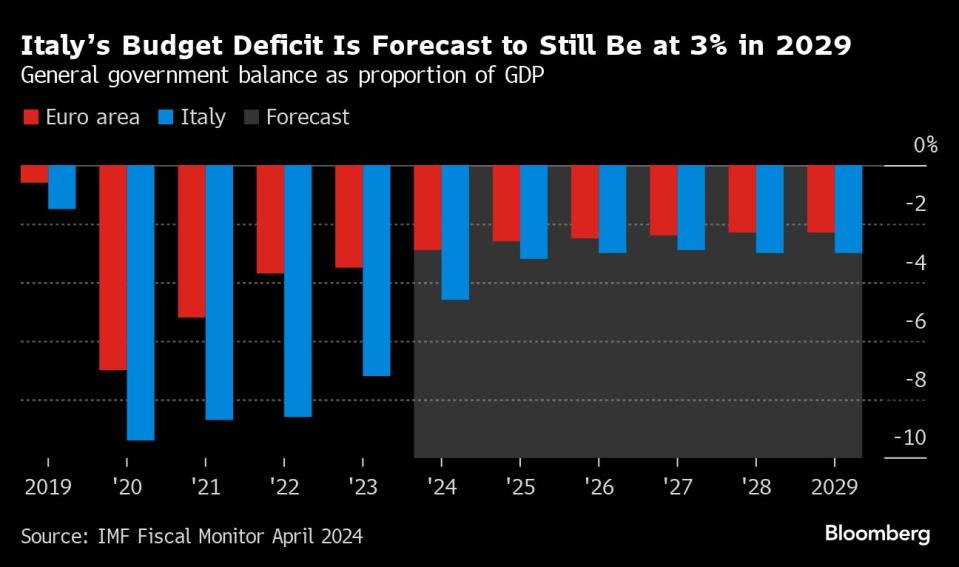

Having previously predicted that borrowings would stay stable, officials last month acknowledged that they will start rising again this year. Italy now faces wider deficits than planned, risking criticism from the European Union.

That shifting trajectory has begun to overshadow the fiscal successes of Meloni’s government, whose approach of mild loosening balanced by overall spending restraint has won the confidence of investors. Italy ended last year with debt at only 137% of output — much lower than originally anticipated.

This week’s BTP Valore sale is the second recent instance when cash-flow challenges appear to have intruded on the government’s fiscal decisions.

Late last month, Meloni also opted to delay a €100 bonus for Italy’s poor. Originally touted for this coming December, the payment will now arrive in 2025 to keep it off this year’s books. The government estimated the cost at €100 million — small change in a multi-billion-euro budget.

Italy has previously faced occasional hiccups in cash management — requiring civil servants to wait months for their salaries, for example — and there’s no suggestion that funding difficulties are the problem here.

Why officials didn’t sell to large investors instead isn’t clear. Two of the people familiar with the government’s thinking speculated that ministers didn’t want to stoke bond yields and rattle voters before European Parliament elections in June. Another person reckoned that the desire to increase consumers’ holdings of Italian debt led to a tactical misjudgment.

If that latter explanation holds true, it would chime with a mixed record under Meloni. Last year, a proposed levy on bank profits rattled investors so much that it wiped billions of euros off their market value. Ministers ultimately watered down the measure to make its impact only marginal.

The Finance Ministry didn’t have an immediate response when contacted by Bloomberg. Earlier this week it said that the government had not expected to replicate the success of previous sales as this was a “special offering” for buyers who didn’t get a chance to participate two months ago.

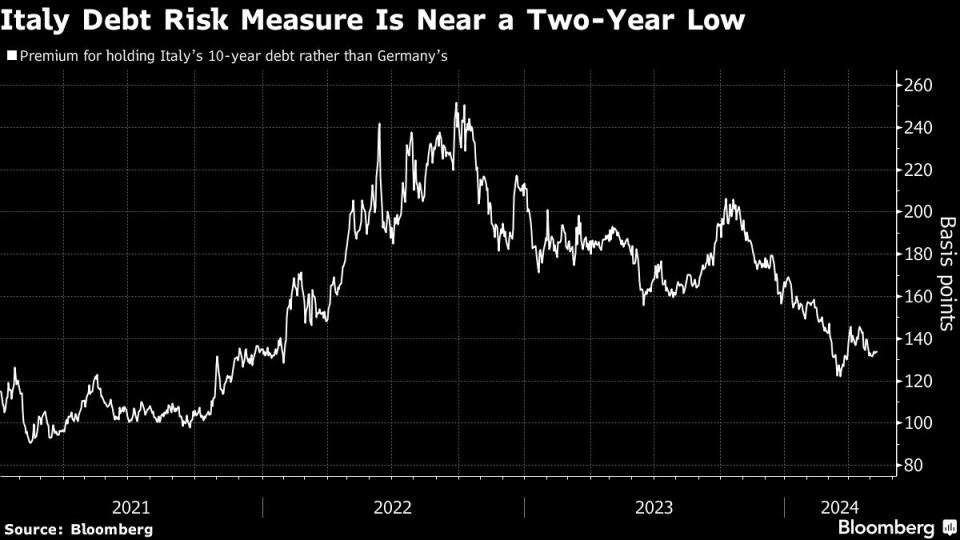

Investors have largely applauded the government’s fiscal performance, matched by stable outlooks from ratings companies. And while retail buying has slowed, that hasn’t put pressure on the nation’s bonds.

The spread between 10-year Italian and German yields is hovering around the lowest in two years at about 130 basis points, an indication of strong appetite from institutional investors for the country’s debt.

The prospect of euro-zone interest-rate cuts as soon as June is also offering a tailwind for the whole region’s sovereign bond market.

“For now, we don’t see the smaller take-up in the May Valore impacting the Tesoro’s plans much,” said Rohan Khanna, head of euro rates strategy at Barclays Plc. “The fact it provided a €20 billion range for its funding plan provides some wriggle room.”

Barclays expects Italy to cancel some of the BTP Valore auctions currently scheduled for the second half, following similar decisions in previous years. In case of any shortfall, the Treasury could stick to those sales and raise up to €15 billion, Khanna said.

That would give Italy some leeway for a coming confrontation with Brussels. With the European Commission scheduled to release recommendations in June to EU countries whose budget deficits exceed the bloc’s limit of 3% of gross domestic product, Rome is bracing for trouble.

The government’s own predictions see Italy’s mammoth debt peaking at 139.8% in 2026. The deficit isn’t seen going below 3% until 2027.

Politically, Meloni is riding high, though at the cost of making expensive promises to voters. She may soon have to decide whether she can afford to keep such pledges at the risk of upsetting the EU, all while managing an easily ruptured coalition.

--With assistance from Aline Oyamada, James Hirai and Alice Gledhill.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.